Digital payments in many African markets are not designed for the realities of small businesses.

Merchants often face:

High upfront costs for POS hardware

Complex onboarding flows requiring technical knowledge

Poor connectivity affecting transaction reliability

Fragmented experiences across payment providers

Low trust in contactless transactions

Many merchants operate in environments where internet connectivity is inconsistent and devices are often low-end Android phones. Existing tools assume reliable connectivity, newer devices, and high digital literacy — assumptions that exclude a large segment of the market.

We needed to design a payment experience that worked within real-world constraints, not ideal conditions.

How might we design a hardware-free payment experience that:

works on low-end smartphones

feels trustworthy for first-time digital payment users

reduces onboarding friction

enables fast transactions in busy environments

scales across merchants, consumers, and partners

builds confidence in contactless payments

These principles guided every decision:

Clarity builds trust

Users need strong feedback signals when money moves.Speed reduces doubt

Transactions should feel immediate and predictable.Familiar patterns reduce the learning curve

Design should feel intuitive even for first-time users.Hardware should not be a barrier

Smartphones should function as POS devices.Systems thinking enables scale

The design system should support future payment methods.

We conducted interviews with merchants and customers to understand how payments happen in everyday contexts.

Many merchants were transitioning from fully cash-based systems and had concerns about:

whether tap-to-pay would work reliably

how quickly they could receive funds

whether customers would trust the experience

how difficult the setup would be

One recurring theme was hesitation toward digital tools perceived as complex or unreliable.

Persona: Amina — Market Trader

Runs a small produce stall

Uses a basic Android device

Has never used a POS system

Prefers tools that work offline

Wants faster checkout without handling cash

Her success metric is simple: complete transactions quickly and confidently during busy hours.

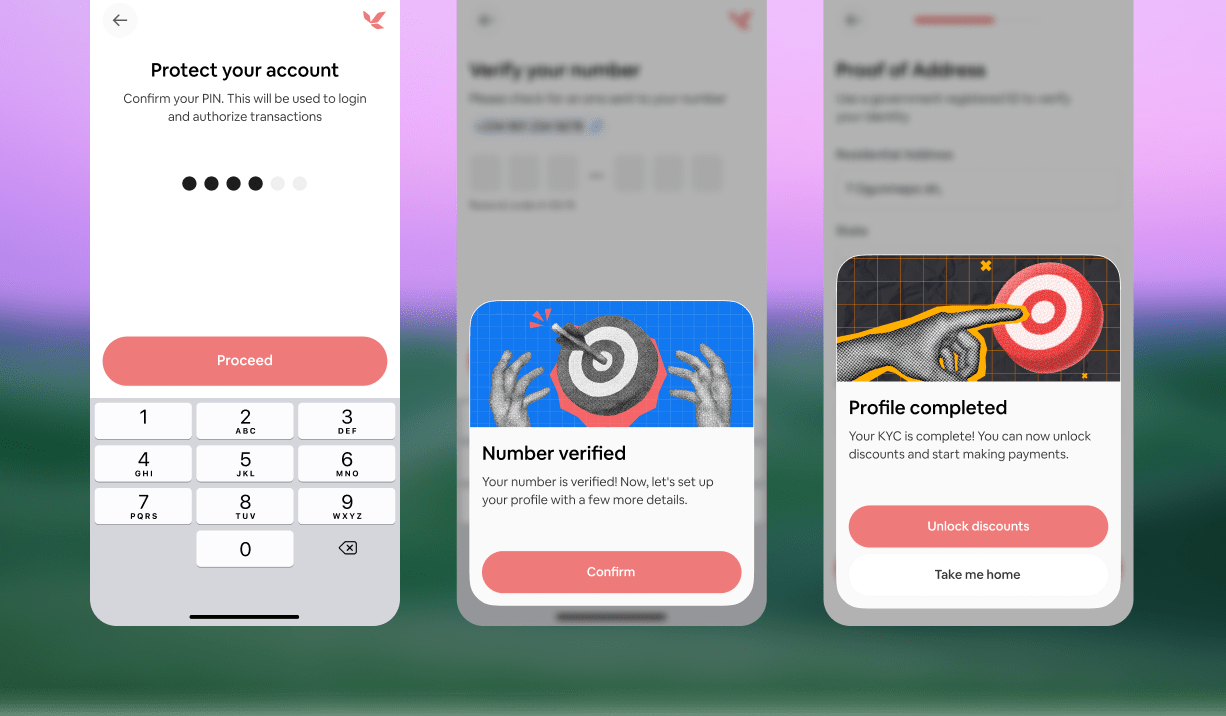

Insights from user interviews directly influenced onboarding simplification and transaction feedback design.

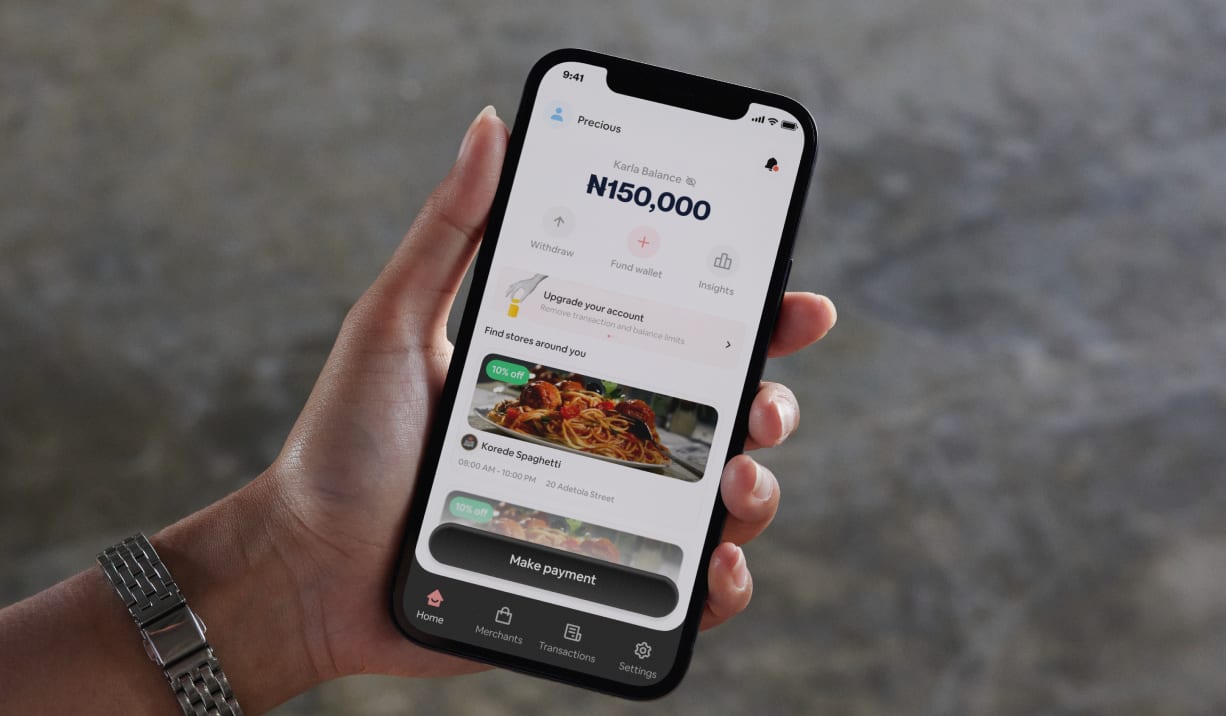

We prioritised the most frequent merchant actions:

Accept payment

View transaction history

Send receipts

Monitor account activity

Less frequent tasks, such as PIN updates and notification settings, were grouped under account-level navigation.

Core navigation structure

Bottom navigation:

Home

Transactions

Summary

Settings

Offline behaviour was considered part of the system design rather than an edge case.

Transactions could queue locally and sync when connectivity resumed, ensuring reliability in unstable network environments.

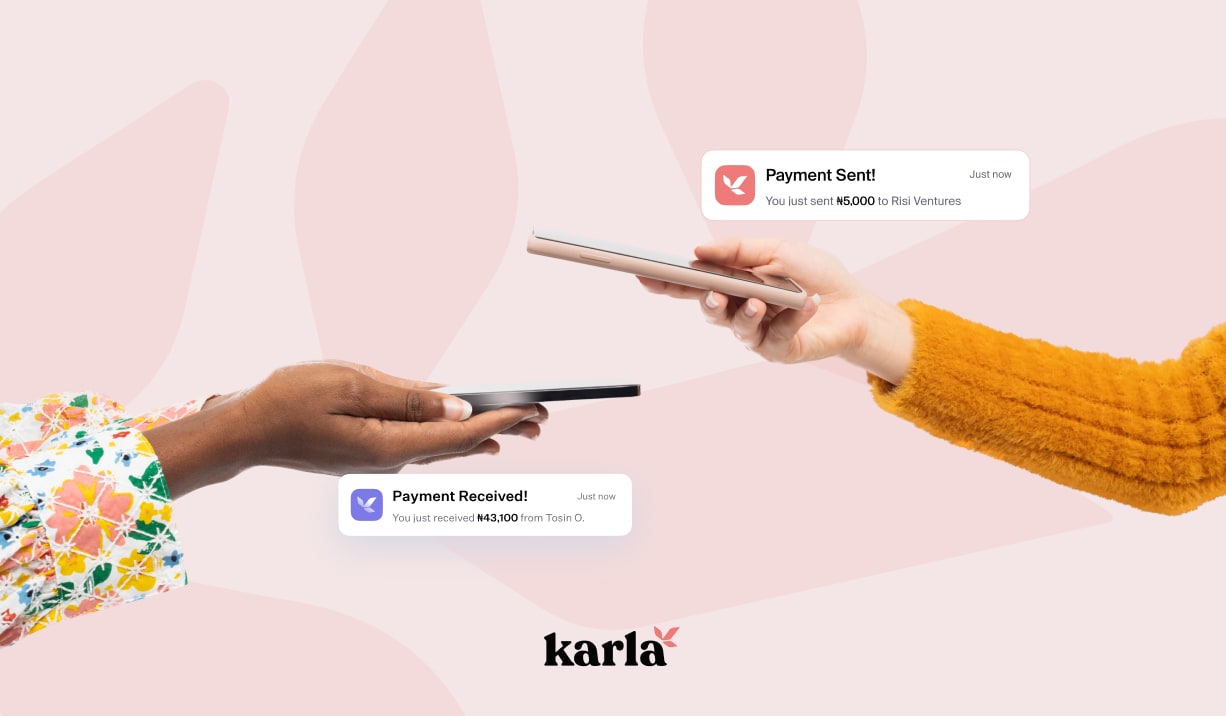

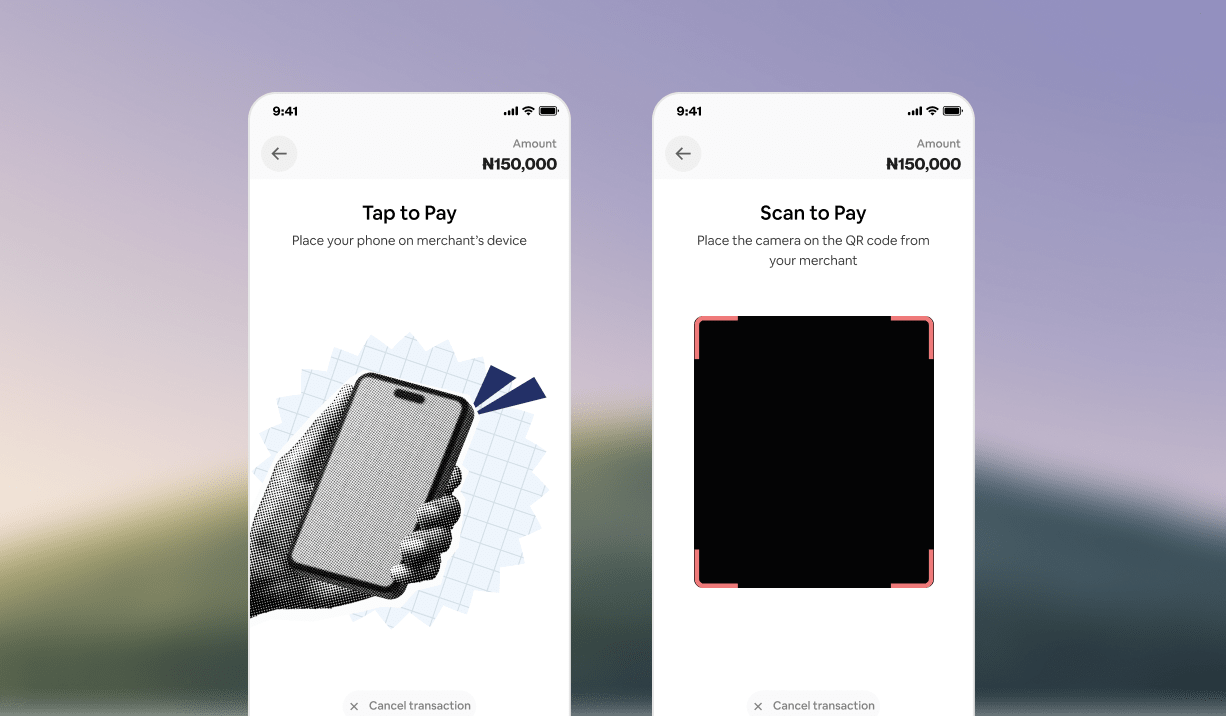

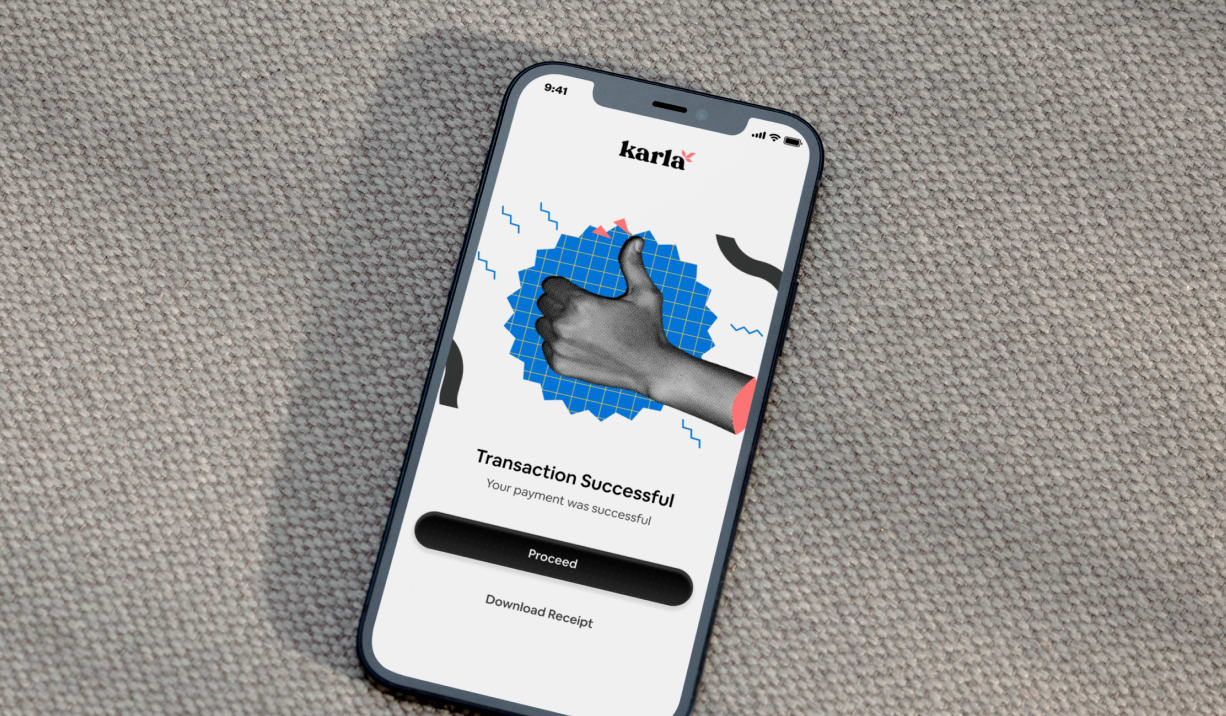

The tap-to-pay interaction needed to communicate three things clearly:

when the phone is ready

when payment is processing

when payment is successful

Small delays or unclear feedback can cause users to repeat transactions or lose trust in the system.

We introduced:

strong visual confirmation states

haptic feedback signals

simplified microcopy

clear transaction summaries

Users immediately understood when a transaction was successful.

Feedback from testing included:

“The green tick helps me know the payment worked right away.”

“I didn’t know my phone could do this.”

I used the Double Diamond framework to structure the product exploration and iteration cycle.

Discover

Conducted interviews with merchants and customers to identify friction in onboarding, trust, and hardware dependency.

Define

Key insights:

merchants needed confidence in transaction success

Onboarding complexity discouraged adoption

Hardware cost created friction for small businesses

unreliable internet requires offline-first thinking

Develop

Explored interaction patterns for tap-to-pay and QR payments.

Tested variations of:

onboarding flows

transaction confirmation states

visual feedback hierarchy

navigation structures

Deliver

Collaborated closely with engineering to ensure NFC flows worked consistently across devices.

Weekly critiques ensured alignment between product, engineering, and business teams.

Iterated onboarding multiple times to improve completion rates.

Within 90 days of launch, Karla demonstrated strong early traction:

200+ daily active users across iOS and Android

$20,000+ transaction volume

40% month-over-month user growth

$3,000 monthly recurring revenue through partnerships

10+ merchant partnerships onboarded

$50,000 marketing grant secured through product positioning

The product helped demonstrate that contactless payments can be viable without dedicated POS hardware.

Karla was also recognised as one of TechCabal’s fintech companies to watch.

Beyond UI delivery, the work influenced broader product direction:

strengthened the positioning of Karla as an infrastructure for contactless payments

improved investor understanding of the product’s scalability

helped define long-term platform capabilities

enabled faster iteration through reusable design patterns

Leadership highlighted the role of design in clarifying the value proposition for both merchants and partners.

Designing Karla meant solving for more than usability; it required building confidence in a new payment behavior.

Because contactless transactions are invisible, users rely heavily on feedback to know what’s happening.

Trust became something we actively designed for.

Clear confirmations, responsive feedback, and simple language helped reduce uncertainty and made the experience feel reliable from the first transaction.